Conquering Retirement Challenges for Women

Looking ahead can help you conquer these unique obstacles.

When it comes to retirement, some women face obstacles that can make saving for retirement a challenge. Women typically earn less than their male counterparts and often take time out of the workforce to care for children or other family members. Added to the fact that women typically live longer than men, retirement money for women may need to stretch even further.1 Despite these challenges, there are a lot of reasons to be hopeful.2

Review your existing situation. Do you want to spend your years traveling together, or do you envision staying closer to home? Are you seeing yourself moving to a retirement community, or do you want to live as independently as you can? Sit down with your spouse, if you’re married, to discuss your visions for retirement.

You can’t see if you’re on track for your goals if you haven’t defined them. And if you find you’re falling short of where you want to be, you can work together to strategize about how you can either get to where you want to go or to adjust your strategy so that it fits your existing situation.1

Get creative. These challenges don’t have to stop you from saving for retirement if you’re willing to get creative. If you plan to or have taken off time from the workforce, try and increase your contributions to your retirement accounts while you are working. If you’re staying home while your spouse works, you may be able to contribute to an individual retirement account.3

Under the SECURE Act, once you reach age 72, you must begin taking required minimum distributions from a Traditional Individual Retirement Account and other retirement plans in most circumstances. Withdrawals from Traditional IRAs are taxes as ordinary income and, if taken before age 59½, may be subject to a 10% federal income tax penalty. Under the CARES Act, the 10% penalty may be waived in 2020. Traditional IRA may be fully or partially deductible, depending on your adjusted gross income.

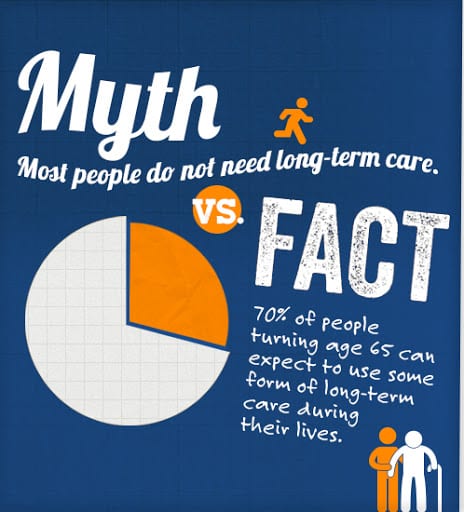

If you’re caregiving for an elderly relative, there are ways to be paid for your time. According to AARP, the Veteran’s Administration or Medicaid may be a potential source of income. Working with a professional who has expertise in this field can help you navigate the complicated medical structure while also helping you earn income for work that you’re doing.3

Get involved. One of the best things you can do is to get involved in conversations about finances. Many women undervalue their knowledge in this area and having regular conversations with your spouse, family, and financial professional can help ensure that you always know where things stand.3

While women may face additional challenges, careful preparation with your financial professional may help you to live a fulfilling retirement.

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.

Traci L. Kovacic is a registered representative of and offers securities through The O.N. Equity Sales Company, Member FINRA/SIPC, One Financial Way; Cincinnati, OH 45242; (513)794-6794

Riverfront Financial and The O.N. Equity Sales Company are unaffiliated companies

Citations

-

CNBC.com, March 6, 2020

-

Entrepreneur.com, August 13, 2020

-

MarketWatch.com, March 6, 2020