Life Insurance

Real Life Stories: Protecting the Future

Protecting the Future

Real Life Stories: Stephen Miller

A mutual friend with a new dog brought Stephen and Katie together. Stephen had headed to his friend’s house to meet the new furry member of the family, and when he got there, he saw Katie playing with dog in the backyard. “Katie was so outgoing,” says Stephen. “She was the nicest person you’ll ever meet.”

That first meeting led to beach outings and concerts, and over time to getting married and thinking about starting a family. It was Katie who suggested they get life insurance. Stephen admits he wasn’t too happy about the idea. They were young and healthy, so he didn’t see the point. Katie, however, convinced him to sit down with insurance professional Rose Goheen, who walked them through the process and presented them with affordable options.

They both decided to get life insurance coverage.

A Growing Family

When the couple welcomed Chase, they decided to reevaluate their life insurance. Given their expanding family and responsibilities, they both bought additional life insurance.

It was during her recovery from giving birth to Reid that Katie realized something was wrong. Her doctor confirmed her suspicion that the abdominal lump she felt was something much more serious. In fact, it was an aggressive form of cancer. Katie, with the love and support of her family, valiantly fought the disease, but just over a year later it claimed this young mom’s life.

She was just 30.

No words can capture the devastation that Stephen and his boys felt at Katie’s loss. “It’s horrible to lose your soul mate and best friend,” he says. “But I have two boys to support, and I want them to know their dad can carry on.”

Life insurance has helped with that process.

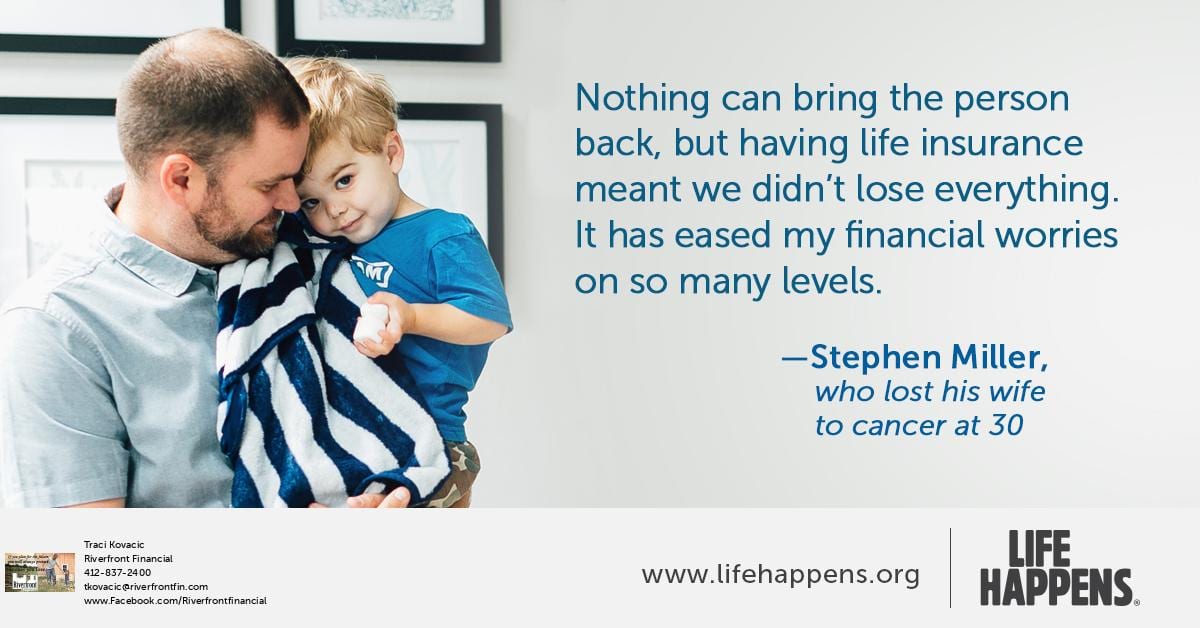

“Nothing can bring Katie back, but having life insurance meant we didn’t lose everything,” he says. “I don’t earn enough alone to afford living in our house. Life insurance has eased my financial worries on so many levels.”

Thinking back to that first meeting with Rose, Stephen says: “Katie was the smarter one. She knew to plan for the future—our future—with life insurance.”

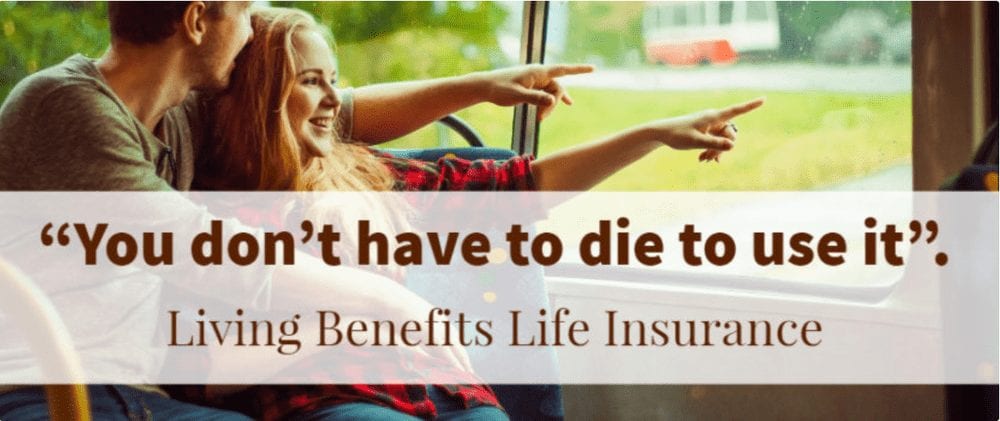

Living Benefits in a Life Insurance policy

What are Living Benefits in a Life Insurance policy?

Quite simply, living benefits are benefits that allow you to access a portion of your policies death benefit while you are still living, if you are diagnosed with a qualifying illness.

In fact, many life insurance policies come with living benefits. The money received can be used any way you choose, from paying hospital bills, to making up for missed work due to illness, and more.

Death may not be the only risk you face on a daily basis. Being diagnosed with a serious illness can also have an adverse effect on your family’s finances, from the high cost of medical bills, to missed work, home nursing care, and much more. Often times, it’s very difficult for families to afford these kinds of expenses with their current income, making a difficult situation even more difficult. That’s where living benefits have advantages.

You may know that life insurance can help fill the income gap for your family and/or beneficiaries if you were to die unexpectedly. Life insurance policies with living benefits add an extra layer of protection if other needs should arise.

To see how life insurance with living benefits can add further protection to your family’s financial strategy and help guard against the unexpected and unknown. Contact us today to learn more about the importance of Life Insurance’s living benefits.

Juanita’s Story

September is Life Insurance Awareness Month!

It’s time for your life insurance check-up.

September is National Life Insurance Awareness Month, so it’s a great time to review your coverage.

If you don’t have any life insurance, you’re not alone. Life insurance is one of those “someday” things for many people – but the cheapest time to buy it is probably today.

There are two kinds of life insurance: term and permanent. Additionally, there are three kinds of permanent life insurance: whole, universal, and variable.

How do these forms of life insurance differ, and how do you find out which type of coverage is right for you?

The way to find out is to look at where you are in life, so that you can assess your current insurance needs. Have you reviewed your insurance lately? Don’t think you need life insurance? If so, consider the following potential factors that may make it a good idea:

*You have a spouse or partner

*You have children

*You have an aging parent or disabled relative who depends on you for support

*Your household depends heavily on your income

*Your retirement savings or pension won’t be enough for your spouse or partner to live on should you pass away

*You own a business, either solely or with partners

*You have a substantial joint financial obligation, such as a personal loan for which another person could be legally responsible after your death

In any of these circumstances, you may require life insurance. If you have coverage, changes in your life may demand an update.

The affordability of life insurance may surprise you. Many people think it is expensive, and so often, it is not. The non-profit insurance education group Life Happens recently

conducted a study about this. More than half the millennial’s contacted for the study thought a $250,000 term life policy would cost $1,000 or more per year. The reality: the a

average annual premium is about $160.1

Life insurance is intended to help your loved ones financially after you die.

The proceeds from a life insurance policy may help your spouse, partner, or family members manage finances if they have to adjust to life without your income.

The death benefit may also be used to meet funeral costs and other final expenses, which may run into the tens of thousands of dollars.

Are you still unsure about buying life insurance, or do you suspect that your current insurance coverage needs to be updated?

Please contact us at (412) 837-2400 or Tkovacic@Riverfrontfin.com and we will be happy to assist you in evaluating all the factors and help you choose an appropriate policy.

Riverfront Financial awarded Best Insurance Agencies in Pittsburgh 2020

This material was prepared by MarketingPro, Inc for use by Traci Kovacic

Traci L. Kovacic is a registered representative of and offers securities through The O.N. Equity Sales Company, Member FINRA/SIPC, One Financial Way; Cincinnati, OH 45242; (513)794-6794

Riverfront Financial and The O.N. Equity Sales Company are unaffiliated companies

Citations.

1 – forbes.com/advisor/insurance/how-much-life-insurance-do-you-really-need/ [8/7/19]