How Much Do You Really Know About Extended and Eldercare?

Separating some eldercare facts from eldercare myths.

How much does eldercare cost, and how do you arrange it when it is needed? The average person might have difficulty answering those two questions, for the answers are not widely known. For clarification, here are some facts to dispel some myths.

True or false: Medicare will pay for your mom or dad’s nursing home care.

FALSE. Medicare is not extended care insurance.1

Medicare Part A will pay the bill for up to 20 days of skilled nursing facility (SNF) care, but after that, you or your parents may have to cover some costs out-of-pocket. After 100 days in a SNF, you will have to cover all costs out of pocket. The only way to “reset the clock” for Medicare coverage of these services is if the patient can somehow go without skilled nursing care for 30 or 60 days or if they require a hospital stay of three full days or longer.1

True or false: A semi-private room in a skilled nursing facility costs about $35,000 a year.

FALSE. The median cost of a semi-private room is now $89,297. A private room in an assisted living facility has a median annual cost of $100,375 annually. A home health aide could run you up to $4385 per month for full-time care. Even if you just need someone to help mom or dad with activities of daily living (ADLs), such as eating, bathing, or getting dressed, the median hourly expense is not cheap: non-medical home aides run about $23 per hour, which at 10 hours a week, means nearly $12,000 a year.2,3

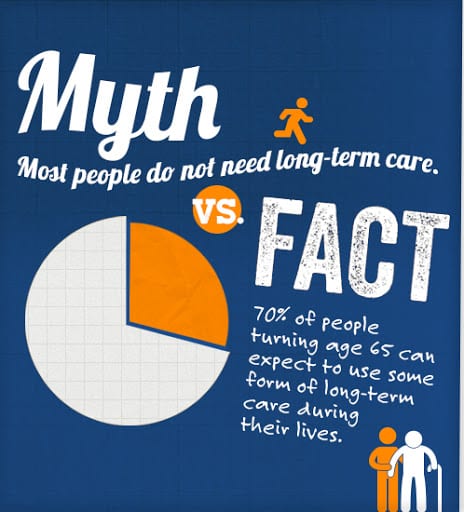

True or false: Only around 40% of Americans aged 65 and older are expected to need extended care.

FALSE. Someone turning 65 today has a 70% chance of needing extended care. That means that by 2030, it’s estimated that around 24 million Americans will need extended care. This is double the current number already receiving care.4,5

True or false: The earlier you buy extended care insurance, the more manageable the premiums.

TRUE. Younger policyholders may pay lower premiums. The best time to consider extended care insurance is when you are healthy. While you may be paying a premium for a longer amount of time, the expense may pale in comparison to paying for unexpected medical costs out of pocket.6

True or false: Medicaid can pay nursing home costs.

TRUE. The question is, do you really want that to happen? While Medicaid rules vary by state, in most instances, a person may only qualify for Medicaid if they have no more than $2,000 in “countable” assets ($3,000 for a couple). A homeowner can even be disqualified from Medicaid for having too much home equity. A primary residence, a primary motor vehicle, personal property, and household items, burial funds of less than $1,500, and tiny life insurance policies (with face values of less than $1,500) are not countable. So, yes, under these economic circumstances, Medicaid may end up paying extended care expenses.7

A little strategizing now could make a big difference in the years to come. Call or email us today to learn more about ways to pay for extended care and discuss your choices. You may need to find a way to address this concern.

Traci L. Kovacic is a registered representative of and offers securities through The O.N. Equity Sales Company, Member FINRA/SIPC, One Financial Way; Cincinnati, OH 45242; (513)794-6794

Riverfront Financial and The O.N. Equity Sales Company are unaffiliated companies

Citations

- Medicare.gov, March 26, 2020

- SeniorLiving.org, June 24, 2020

- APlaceForMom.com, May 11, 2020

- AmericanActionForum.org, February 18, 2020

- LongTermCare.gov, July 23, 2020

- Forbes.com, April 17, 2020

- LongTermCare.ACL.gov, July 23, 2020

This material was prepared by MarketingPro, Inc., and does not necessarily represent the views of the presenting party, nor their affiliates. This information has been derived from sources believed to be accurate. Please note – investing involves risk, and past performance is no guarantee of future results. The publisher is not engaged in rendering legal, accounting or other professional services. If assistance is needed, the reader is advised to engage the services of a competent professional. This information should not be construed as investment, tax or legal advice and may not be relied on for the purpose of avoiding any Federal tax penalty. This is neither a solicitation nor recommendation to purchase or sell any investment or insurance product or service, and should not be relied upon as such. All indices are unmanaged and are not illustrative of any particular investment.