A Roth IRA’s Many Benefits

Why do so many people choose them over traditional IRAs?

Provided by Traci Kovacic

The IRA that changed the whole retirement savings perspective. Since the Roth IRA was introduced in 1998, its popularity has soared. It has become a fixture in many retirement planning strategies because it offers savers so many potential advantages.

The key argument for going Roth can be summed up in a sentence: Paying taxes on your retirement contributions today may be better than paying taxes on your retirement savings tomorrow.

Think about it. Would you rather pay taxes today or wait 10 years and see where the tax rates end up? With that in question in mind, here are some of the potential benefits associated with opening and contributing to a Roth IRA.

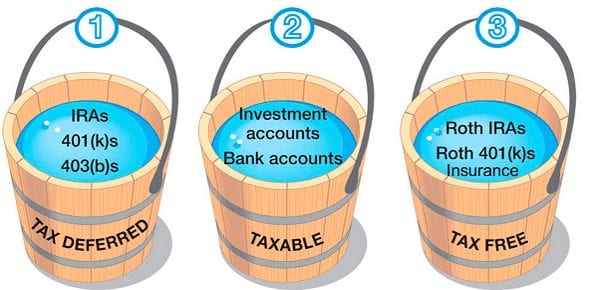

What you see is what you get. Roth IRA contributions are made with after-tax dollars, and any potential earnings on investments within a Roth IRA are NOT subject to income tax or included in the account owner’s income. Instead, they accumulate on a tax-deferred basis and are tax-free when withdrawn from the Roth if the distribution is qualified.1

You can arrange tax-free retirement income. Roth IRA earnings can be withdrawn tax-free as long as you are 59½ or older and have owned the account for at least 5 years. The IRS calls such tax-free withdrawals qualified distributions.2

Withdrawals don’t affect taxation of Social Security benefits. If your provisional income is between $25,000 and $34,000 — or $32,000 and $44,000 for joint filers — then your Social Security benefits may be taxed if you take withdrawals before your full retirement age. Luckily, a qualified distribution from a Roth IRA doesn’t count as taxable income, which may be a means of avoiding taxation on your social security benefit.3,4

You have until your tax-filing deadline to make a Roth IRA contribution for a given tax year. For example, IRA contributions for the 2020 tax year may be made up until April 15, 2021. While April 15 is the annual deadline, many IRA owners who make lump sum contributions for a given tax year make them as soon as that year begins, not in the following year. Making your Roth IRA contributions earlier gives the funds in the account more time to potentially grow. Remember, though that Roth IRA contributions cannot be made by taxpayers with high incomes. In 2020, the income phaseout limit was $139,000 for single filers and $206,000 for married couples who file jointly.5

Who can open a Roth IRA? Anyone with earned income (and that includes a minor).

How much can you contribute to a Roth IRA annually? The combined annual contribution limit to all of your traditional and Roth IRAs is $6,000 for 2019 and 2020 ($7,000 if you’re age 50 or older), but income limits may reduce or eliminate your ability to contribute. To sweeten the deal even further, you can keep making annual Roth IRA contributions all your life.6

All this may have you thinking about opening up a Roth IRA. A chat with the financial professional you know and trust may help you evaluate whether a Roth IRA is right for you, given your particular tax situation and retirement horizon.

Have you experienced a life change recently like having a baby or getting a new…

Go out into your yard and dig a big hole. Every month, throw $50 into…

Qualified distributions are used to pay for education expenses at eligible schools and institutions. If withdrawals…

Protecting the Future Real Life Stories: Stephen Miller A mutual friend with a new dog…

{kind=link}

{kind=link}